Investor relations > About us > Market environment

Market environment

ED Invest S.A. operates in Poland within the property market, which remains closely linked to the country’s overall economic health. Key factors influencing the property development and construction sectors include GDP growth, inflation, interest rates, and government policy regarding the housing market and government programmes.

According to official data from the Central Statistical Office (GUS) from mid-May this year, in Q1 2026 Poland’s gross domestic product (GDP) reached 4.5%, an increase of 0.5% compared to the previous quarter (after adjusting for seasonal factors), whilst on an annual basis it rose by 3.4% in real terms. And although this result is slightly below market expectations (with growth forecast at around 3.7%), these figures confirm Poland’s sustained economic growth

Housing market

The first quarter of 2026 saw the Polish residential property market continue the recovery that began towards the end of the previous year. The sector has moved beyond a wait-and-see phase and, driven by factors such as rising GDP growth, access to finance, rising average wages, easing monetary policy, a slight rise in inflation and unemployment, it definitively moved into a phase of high buyer activity (with particular emphasis on those who had held off on decisions for most of 2025).

Between January and March 2026, building permits were issued for 45,900 flats (an increase of 11% compared to the same period last year), bringing the total number of residential units available on the primary market in Poland to approximately 58,900.

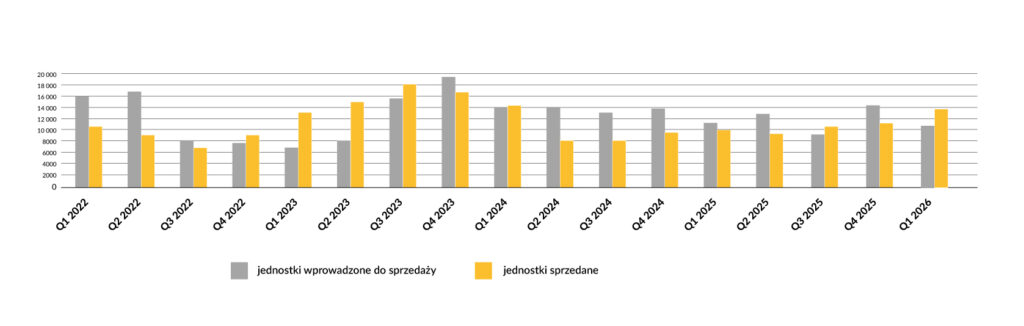

During this period, developers in the seven largest urban areas (Warsaw, Kraków, Wrocław, the Tri-City, Poznań, Łódź and Katowice) launched 10,300 new flats onto the market (27% fewer than in the previous quarter), whilst over 12,900 units were sold (11.1% more than in Q4 2025).

Chart 1. Quarterly supply and demand report for Q1 2026 (aggregated data for six markets: Warsaw, Kraków, Wrocław, the Tri-City, Poznań and Łódź).

Source: JLL Report: “The Residential Market in Poland | Research Poland, Q1 2026”

Availability of mortgage credit

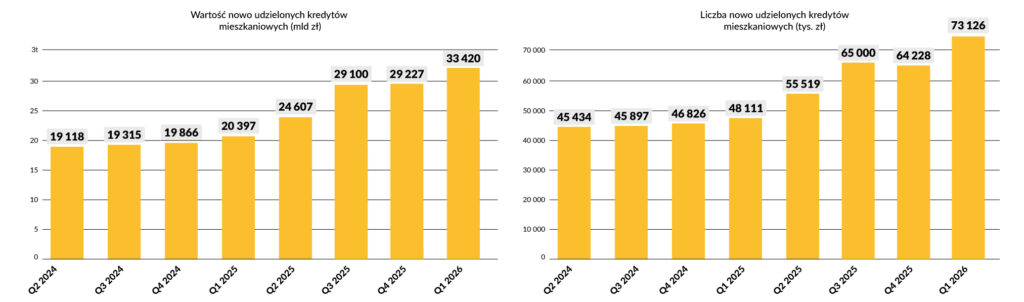

The results for the first quarter of 2026 maintained and reinforced the trend of a recovery in lending seen over the last three quarters. Between January and March of this year, over 144,000 applications were submitted (January – 36,600, February – 44,500, March – 63,310), representing a 14% increase quarter-on-quarter. The total number of mortgage loans granted in Poland in the first three months of 2026 amounted to 73,126 (a record increase of 13.85% compared to Q4 and the highest figure in 18 years) and totalled over PLN 33,420 billion. (an increase of 14.34% quarter-on-quarter and as much as two-thirds compared to Q1 of last year).

The average value of housing loans granted in Q1 2026 was PLN 457,260 and, although this was only 0.5% higher than in the previous quarter, it rose by 8% compared to Q1 2025.

The key factors driving the unprecedented rise in demand for mortgage financing were an improvement in Poles’ creditworthiness [in March, the Monetary Policy Council (RPP) cut key interest rates once again, bringing the rate down from 4.00% to 3.75%], rising wage growth and market competition among banks through consistent reductions in lending margins and the relaxation of requirements for borrowers.

Furthermore, such a dramatic shift in customer behaviour also stems from fears that the era of cheap financing is coming to an end, a sense of geopolitical uncertainty caused by the conflict in the Middle East and rising oil prices on global markets, and the spectre of a return to inflation.

Chart 2. The total value and number of new mortgage loans granted in the first quarter of 2026. (in thousands).

Source: AMRON-SERFiN Report – National Report on Mortgage Loans and Property Transaction Prices No. 1/2026

Apartment prices

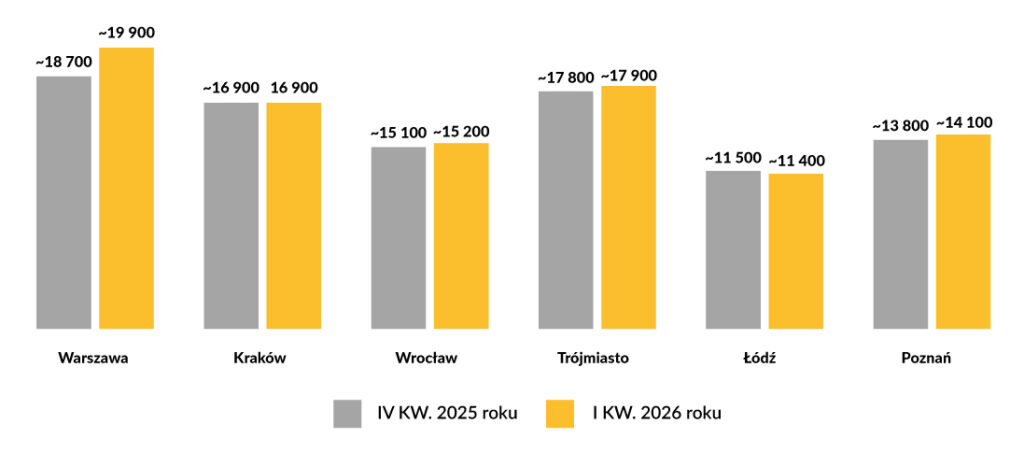

The flat sales market in the first quarter of 2026 showed similar price trends to the previous quarter – most cities recorded only slight changes in average transaction prices (over the year as a whole, by just a few per cent, i.e. from -0.5% to +1%). The exception is Warsaw, which continues to hold the status of the most expensive market – here, a price increase of over 3.5% was recorded.

It is worth noting here that the asking price and the transaction price are two different things, and the difference between them reflects the extent of the negotiations.

And so, the average asking price per square metre in Q4 2025 was: in Warsaw ~PLN 19,900/m² (approx. +3.7% q/q), Kraków ~PLN 16,900/m² (unchanged MoM), Wrocław ~PLN 15,200/m² (+0.5% MoM), Łódź ~PLN 11,400/m² (-0.5% MoM), the Tri-City ~PLN 17,900/m² (approx. +0.5% MoM) and Poznań ~PLN 14,100/m² (approx. +1.0% MoM).

In overall annual terms, major regional cities saw slight price fluctuations – mainly in the single digits. In most cases, these were changes in the average asking price on both a quarterly and annual basis.

Chart 2. Average prices of flats on the primary market in Q1 2026 (in PLN/m², inclusive of VAT, in developer-finished standard).

Source: JLL Report: “The Residential Market in Poland | Research Poland, Q1 2026”

Developer activity – demand vs. supply

The sustained growth in demand in the first quarter of 2026 in the housing market, driven in part by improved mortgage financing conditions, is a sign to most developers that the coming quarters of 2026 should be equally successful. The ongoing upturn in the primary market for new-build flats has resulted in further record results.

The total number of flats sold across the seven main markets exceeded 12,800 units, representing an 11.1% increase compared to Q4 2025 and a 30% year-on-year rise.

In Warsaw alone, over 4,239 new flats were sold, a result 12.8% higher than in the previous quarter and 12.1% above the average quarterly sales figure for the last five years, which stood at 3,781 units. This is also the best quarterly sales result in two years, i.e. since the end of the impact on the market of the government’s ‘Safe 2% Loan’ subsidy scheme.

At the same time, 2,850 flats were launched on the primary market in Warsaw during this period, marking the first time that the figure was as much as 29.7% lower than in the previous quarter. Overall, as a result of increased sales and a decline in new supply, the total number of new flats available on the market in March 2026 in Warsaw reached 15,255 units, down 8.6% compared to December 2025 and the lowest level since September 2024

Forecasted changes

To summarise the first quarter of 2026, it must be said that, despite some unfavourable factors and the lack of government support in the form of subsidy or tax relief schemes, the construction sector enjoyed a positive start to the year. As always, flats with a floor area of 40–60 m² were the most popular among buyers, and these were also the most numerous on the market. Forecasts for the rest of the year indicate that this trend will continue.

It is unclear how much of a negative impact rising inflation, the anticipated slowdown in wage growth, or the current war in the Gulf will have on the construction industry. Furthermore, banks are already forecasting an increase in mortgage interest rates and a halt to the National Bank of Poland’s cycle of rate cuts. There is no doubt that the costs of new construction projects will also rise due to higher prices for materials and fuel. Prices for newly launched flats must therefore rise, and their total number is likely to start falling.

The fact that the number of building permits granted is 50% higher than the number of construction projects actually started confirms that the industry is actively securing its project portfolios, but is holding off on launching them until the market has absorbed the surplus of completed properties that still exists. This situation should be described as ‘waiting for readiness’ .

And although all the factors mentioned above may have a restrictive effect on supply, both in decision-making processes and in the implementation of new projects, it should be remembered that the market operates according to its own laws.